Swiss Accounting Requirements Explained: Complete Guide

- Nov 23, 2025

- 6 min read

Updated: Dec 16, 2025

More than 90 percent of american companies expanding into Switzerland underestimate just how strict Swiss accounting requirements can be. Managing precise financial records is not only a matter of good practice but a legal necessity, with severe penalties for businesses that fall short. Understanding these detailed rules helps protect your company from costly missteps and gives you a clear roadmap for setup, reporting, and compliance in the Swiss business environment.

Table of Contents

Key Takeaways

Point | Details |

Accounting Thresholds | Businesses exceeding CHF 500,000 in annual sales must maintain detailed accounting records, while smaller entities may utilize simplified methods. |

Mandatory Documentation | Companies must keep comprehensive financial records for a minimum of 10 years, ensuring true and fair representation of their financial health. |

Audit Requirements | Firms exceed specific benchmarks are required to undergo ordinary audits, with varying requirements for smaller companies. |

Compliance and Penalties | Timely financial reporting is critical, with significant penalties for non-compliance, emphasizing the need for professional accounting support. |

Swiss Accounting Requirements Defined and Demystified

Navigating the intricate landscape of Swiss accounting requirements demands precision and strategic understanding. According to kmu.admin.ch, Swiss legal entities and sole proprietorships face specific mandatory accounting obligations that vary based on annual sales volume.

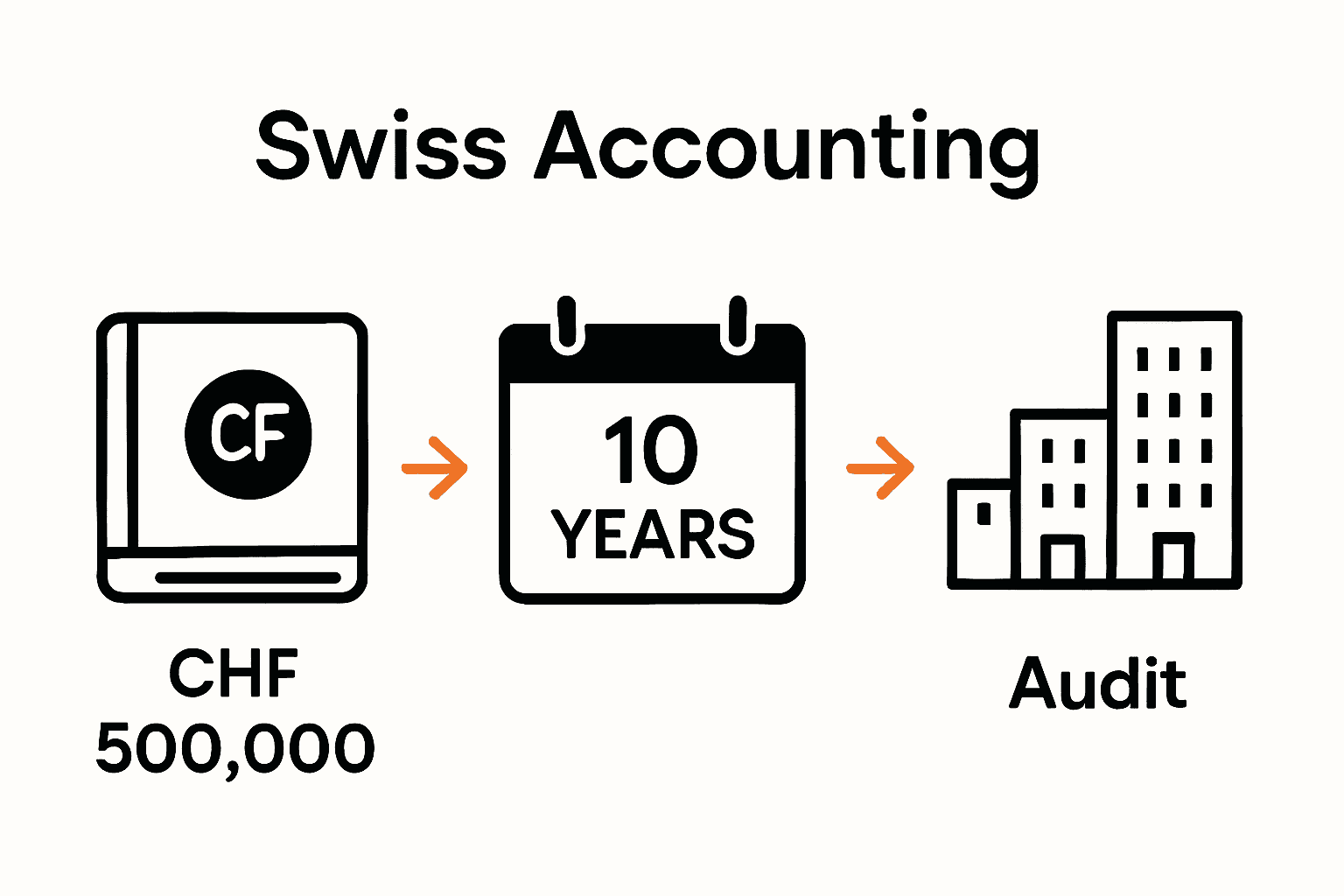

Accounting Threshold Requirements are clearly defined in Swiss regulations. Businesses with annual sales exceeding CHF 500,000 must maintain comprehensive accounting records, which include:

Detailed inventory documentation

Comprehensive balance sheet

Profit and loss statement

Minimum 10-year document retention

For smaller enterprises generating less than CHF 500,000 annually, simplified accounting methods are permitted. Swiss GAAP FER provides nuanced accounting and reporting recommendations specifically tailored for small and medium-sized organizations, offering a modular framework that ensures transparent financial reporting.

The Swiss accounting ecosystem prioritizes accuracy and transparency. Companies must implement robust financial tracking systems that comply with national standards, maintaining meticulous records that reflect true operational and financial performance. Compliance is not optional but a legal requirement, with potential significant penalties for inadequate financial documentation.

To successfully navigate these requirements, businesses should consider engaging professional accounting services familiar with Swiss regulatory standards. Company Formation Checklist Switzerland: Step-by-Step Guide can provide additional insights into establishing compliant financial practices when operating in Switzerland.

Key Accounting Standards and Reporting Rules

Swiss accounting standards represent a sophisticated framework designed to ensure financial transparency and precision. FER (Foundation for Accounting and Reporting Recommendations) provides the foundational principles through Swiss GAAP FER 1, which emphasizes creating meaningful financial reporting that delivers a true and fair view of an organization’s financial position.

Key Reporting Principles encompass several critical elements that businesses must integrate into their financial documentation:

Consistent accounting practices

Transparent financial statements

Comprehensive disclosure requirements

Comparative financial information

PwC Switzerland highlights the importance of staying current with evolving standards, noting recent updates like Swiss GAAP FER 28 on government grants effective January 1, 2024. These standards are not static but dynamically adapt to changing business environments and international financial reporting trends.

The Swiss accounting standards prioritize comprehensive documentation that goes beyond mere number reporting.

Companies must present financial information that tells a coherent story of their economic activities, ensuring stakeholders can understand the organization’s financial health, operational strategies, and potential future trajectories.

For international businesses operating in Switzerland, understanding these nuanced reporting rules is crucial. Consulting with local accounting professionals who specialize in Swiss Company Registration Process can provide invaluable guidance in navigating these complex regulatory requirements effectively.

Mandatory Record-Keeping and Documentation Duties

kmu.admin.ch reveals that Swiss accounting regulations impose rigorous documentation requirements that businesses must meticulously follow. The Swiss Code of Obligations mandates comprehensive record-keeping practices designed to ensure financial transparency and accountability across all organizational structures.

Documentation Requirements for Swiss businesses include maintaining several critical financial records:

Detailed inventory documentation

Comprehensive balance sheet

Profit and loss statements

Comprehensive financial transaction logs

Minimum 10-year document retention

Swiss GAAP FER emphasizes that these documentation duties go beyond simple record preservation. The standards require companies to maintain records that provide a true and fair view of their financial position, ensuring each document tells a clear and accurate story of the organization’s financial health.

The implications of non-compliance are significant. Companies failing to maintain proper documentation risk substantial penalties, potential legal challenges, and loss of business credibility.

These record-keeping obligations apply universally, regardless of company size or sector, making professional accounting support crucial for navigating these complex requirements.

For international businesses, understanding these intricate documentation duties can be challenging. Consulting with experts who specialize in Swiss Company Formation Checklist can provide invaluable guidance in establishing robust accounting practices that meet Swiss regulatory standards.

Audit Requirements and Company Size Thresholds

Swiss regulatory frameworks establish nuanced audit requirements that dynamically adapt to a company’s size and operational complexity. kmu.admin.ch provides clear guidelines for determining audit obligations based on specific organizational metrics.

Audit Threshold Criteria for Swiss companies are precisely defined. A company becomes subject to an ordinary audit if it exceeds two of the following benchmarks for two consecutive years:

Balance sheet total of CHF 20 million

Annual sales reaching CHF 40 million

250 or more full-time employees

Smaller enterprises enjoy more flexible regulations. Companies with fewer than ten full-time employees can potentially opt out of comprehensive auditing with appropriate shareholder approval.

This graduated approach ensures that regulatory requirements remain proportional to organizational scale and complexity.

PwC Switzerland highlights the recent updates to consolidated financial statement requirements, effective January 1, 2024. These evolving standards demonstrate Switzerland’s commitment to maintaining rigorous yet adaptive financial reporting frameworks that balance regulatory oversight with business flexibility.

For international businesses navigating these intricate requirements, professional guidance becomes essential. Swiss Company Registration Process experts can provide critical insights into structuring your organization to meet these precise audit and reporting standards effectively.

Compliance Timelines, Penalties, and Common Pitfalls

kmu.admin.ch reveals critical insights into Swiss financial reporting compliance, emphasizing the stringent timelines and potential consequences for businesses. Companies must navigate a complex landscape of regulatory requirements that demand precision and timeliness in financial documentation.

Key Compliance Deadlines for Swiss companies typically range from six to nine months after fiscal year-end, with variations depending on specific cantonal regulations:

Precise financial statement preparation

Comprehensive documentation submission

Internal and external audit completion

Shareholder reporting requirements

Timely tax declaration submissions

FINMA and SIX Exchange Regulation have significantly reinforced financial reporting supervision, highlighting several common pitfalls that businesses must carefully avoid:

Inadequate financial disclosures

Non-compliance with accounting standards

Incomplete documentation

Missed reporting deadlines

Inconsistent accounting practices

The implications of non-compliance can be severe. Companies may face substantial financial penalties, legal challenges, and potential loss of business credibility. Regulatory bodies demonstrate zero tolerance for systematic reporting failures, making professional accounting support not just recommended but essential.

International businesses must be particularly vigilant. Consulting experts who specialize in Swiss Company Formation Checklist can provide critical guidance in developing robust compliance strategies that meet Switzerland’s exacting financial reporting standards.

Master Swiss Accounting with Expert Support for Your Business

Swiss accounting requirements are complex and demanding. If you struggle with maintaining detailed inventory records, meeting the minimum 10-year document retention, or navigating audit thresholds tied to your company size, you are not alone. These challenges can cause costly compliance issues and stress for international entrepreneurs unfamiliar with local regulations. The need for consistent accounting practices and transparent financial statements is critical for your company’s success and credibility.

Take control now with professional guidance from RPCS The platform offers comprehensive assistance including legal documentation, notarization, company registration, and expert accounting services tailored to Switzerland’s strict standards. Stay ahead of deadlines and avoid penalties by partnering with specialists who understand the nuances of Swiss GAAP FER and audit requirements. Explore the Swiss Company Registration Process and use the Company Formation Checklist Switzerland: Step-by-Step Guide to ensure your business is fully compliant. Act today to secure your smooth setup and long-term success in Switzerland’s stable and favorable business environment.

Frequently Asked Questions

What are the accounting threshold requirements for businesses in Switzerland?

Businesses with annual sales exceeding CHF 500,000 must maintain comprehensive accounting records, including detailed inventory documentation, a comprehensive balance sheet, and a profit and loss statement with a minimum 10-year document retention.

What accounting standards are followed in Switzerland?

Swiss accounting standards are primarily based on Swiss GAAP FER (Generally Accepted Accounting Principles), which emphasize creating meaningful financial reports that provide a true and fair view of an organization’s financial position.

What are the mandatory record-keeping and documentation duties for Swiss businesses?

Swiss businesses must maintain several critical records, including detailed inventory documentation, a comprehensive balance sheet, profit and loss statements, comprehensive financial transaction logs, and retain these documents for at least ten years.

What are the audit requirements based on company size in Switzerland?

A company must undergo an ordinary audit if it exceeds two of the following benchmarks for two consecutive years: a balance sheet total of CHF 20 million, annual sales of CHF 40 million, or having 250 or more full-time employees. Smaller companies may opt-out of audits under certain conditions.

Recommended

Comments